The State of Markets: “Regime Change? Or Buy The Dip?”

After months of optimism, the mood in markets has shifted this past week. That started last Friday, with Trump threatening China with higher tariffs. Equities sold off and Treasuries rallied on the news. Risk aversion then continued yesterday on concerns about the health of some US commercial banks. With that, US Treasury yields are trading at multi-month lows, having broken out of their pennant formation last month (see 10 year yields in the chart below).

The key question, therefore, is: Has the risk appetite regime changed? And, with sharp reversals in key asset prices this week (like silver, which is down 5% today), how worried should we be? Or – is recent weakness merely a short term wobble, and therefore an opportunity to buy the dip?

Next week the US macro calendar will be dominated by the September CPI report (out on Friday, having been delayed due to the shutdown). While an exception has been made for CPI, other government data releases will likely remain suspended. That will probably include Monday’s Conference Board leading index (which relies heavily on government data inputs, like building permits and jobless claims). US S&P manufacturing & service sector PMIs are expected to go ahead (and are initial estimates for October). PMI data for other economies will also be released next Friday.

Key events include (i) China’s 15th five-year Communist Party plan (a meeting about economic policy and reform, from Monday to Thursday); (ii) a PBoC policy decision (Monday); and (iii) the ECB/BIS/CEPR 2025 conference in Frankfurt (Monday & Tuesday). Elsewhere there are speeches from key ECB and BoE central bankers, while the Fed enters into its communications blackout phase. Earnings season remains ongoing, with reports from key US companies including Amazon, Intel, Netflix & GM. Please see below for a full list of next week’s key data and events.

Key chart: US 10 year Treasury yield (%, shown with key moving averages)

Upcoming Important Data/Events This Week:

Upcoming Important Data/Events This Week:

|

Events: |

NB The US government shutdown is ongoing – and delaying the release of certain data points. China's Communist Party holds plenum on its 15th five-year plan (Mon to Thurs); PBOC policy decision (Mon, 2am); ECB/BIS/CEPR 2025 conference ‘WE_ARE_IN Macroeconomics and Finance’ in Frankfurt (Mon & Tues); Lagarde to speak in Frankfurt at ‘Finance & Future’ summit (Wed, 1:25pm). |

|

Monday: |

Chinese GDP (Q3, 3am); US Conference Board leading index (Sept, 3pm). |

|

Tuesday: |

N/A |

|

Wednesday: |

UK headline & core CPI, RPI & PPI (Sept, 7am). |

|

Thursday: |

US existing home sales (Sept, 3pm). |

|

Friday: |

US headline & core CPI (Sept, 1:30pm); Japanese headline & core CPI (Sept, 12:30am); manufacturing & service sector PMIs (all October first estimate) for Japan (1:30am), France (8:15am), Germany (8:30am) & Eurozone (9am) & US (2:45pm). |

|

Key earnings: |

Netflix, Lockheed Martin, General Motors, L'Oreal (Tues); Tesla, IBM, Hermes International (Wed); Amazon.com, Blackstone, Intel, Ford Motor (Thurs). |

Key Research

Longview on Friday, 17th October 2025:

“No Smoke Without Fire”

As we laid out in our latest monthly Tactical publication on 1st October (“Speculative Excess, Froth and Euphoria”):

“Signs of frothiness, speculative excess and euphoria continue to grow in the US

equity market. Some of those signs have spilt out across the broader global financial landscape. This past month’s price action has been especially exuberant (in parts of the market).”

Shortly after that (last Friday), the market then fell sharply (S&P500 down 2.7% on the session; NDX100 -3.5%). That was initially attributed to Trump’s China tariffs threat. Over last weekend (after Friday’s fall), he then set out to reassure the markets, “Don’t worry about China, it will all be fine!” which (somewhat) contributed to a bounce earlier this week. Since then, though, equities have struggled, and traded inside the breadth of last Friday’s pullback (fig 2). Added to which, the macro reason to sell has evolved, with the market now focused on the regional banks, private credit woes and specifically Jefferies, Zions bank and one or two other regionals.

Key North American Macro Data & Events:

|

Events: |

NB The US government shutdown is ongoing – and delaying the release of certain data points. Fed’s external communications blackout (all week); Bank of Canada business outlook Q3 (Mon, 3:30pm). |

|

Monday: |

Canadian industrial product & raw material price index (Sept, 1:30pm); US Conference Board leading index (Sept, 3pm). |

|

Tuesday: |

US Philadelphia Fed service sector activity (Oct, 1:30pm); Canadian headline & core CPI (Sept, 1:30pm). |

|

Wednesday: |

N/A |

|

Thursday: |

Canadian retail sales (Aug, 1:30pm); US weekly jobless claims (1:30pm); US Chicago Fed national activity (Sept, 1:30pm); US existing home sales (Sept, 3pm); US Kansas City Fed manufacturing sector activity (Oct, 4pm). |

|

Friday: |

US headline & core CPI (Sept, 1:30pm); US S&P manufacturing & service sector PMIs (October first estimates, 2:45pm); US new home sales (Sept, 3pm); US Michigan Sentiment (October final estimate, 3pm); US Kansas City Fed service sector activity (Oct, 4pm). |

|

Key earnings: |

Netflix, GE Aerospace, Coca-Cola, Philip Morris, Rtx Corp, Texas Instruments, Intuitive Surgical, Danaher, Capital One Financial, Lockheed Martin, Chubb, Northrop Grumman, 3M, Elevance Health, General Motors, Nasdaq Inc, PACCAR (Tues); Tesla, IBM, Thermo Fisher Scientific, AT&T, Lam Research, GE Vernova LLC, Amphenol, Boston Scientific, KLA Corp, CME Group, O’Reilly Automotive, Moody’s, United Rentals, Hilton Worldwide, Kinder Morgan (Wed); Amazon.com, T-Mobile US, Blackstone, Intel, Union Pacific, Honeywell, Newmont Goldcorp, Norfolk Southern, Digital, Freeport-McMoran, Roper Technologies, Valero Energy, Ford Motor (Thurs); HCA, General Dynamics, Illinois Tool Works (Fri). |

Fig B: US headline & core CPI (Y-o-Y %)

Key European Macro Data & Events

Key European Macro Data & Events

|

Events: |

ECB/BIS/CEPR 2025 conference ‘WE_ARE_IN Macroeconomics and Finance’ in Frankfurt (Mon & Tues); speeches by ECB’s Schnabel in Frankfurt (Mon, 9am & 3pm), Lane in Frankfurt (Tues, 8am), Lagarde at Norges Bank climate conference (Tues, 12pm), Kocher in Vienna (Tues, 2:30pm), Lagarde in Frankfurt at ‘Finance & Future’ summit (Wed, 1:25pm); ECB’s pre-rate decision quiet period (23rd to 29th). |

|

Monday: |

German PPI (Sept, 7am); Eurozone ECB current account (Aug, 9am); Italian current account balance (Aug, 9:30am); Eurozone construction output (Aug, 10am). |

|

Tuesday: |

N/A |

|

Wednesday: |

French retail sales (Sept). |

|

Thursday: |

French INSEE business & manufacturing confidence (Oct, 7:45am); Spanish home sales & mortgage approvals (Aug, 8am); Spanish trade balance (Aug, 9am); Eurozone consumer confidence (October first estimate, 3pm). |

|

Friday: |

French consumer confidence (Oct, 7:45am); Spanish PPI (Sept, 8am); Spanish unemployment rate ( Q3, 8am); HCOB manufacturing & service sector PMIs for France (8:15am), Germany (8:30am) & Eurozone (9am) – all October first estimates. |

|

Key earnings: |

ASSA ABLOY B, L'Oreal (Tues); SAP, Hermes International (Wed); Atlas Copco, Unilever, Relx, Vinci, Thales (Thurs); Safran, Sanofi, Eni SpA (Fri). |

Fig C: Eurozone consumer confidence (index)

Key UK Macro Data & Events

Key UK Macro Data & Events

|

Events: |

Speeches by BOE’s Cleland (Tues, 2pm), deputy governor Woods at Annual City Banquet (Wed, 9pm), Hall (Thurs, 2pm), Woods is a panellist at the FCA forum (Fri, 10:15am). |

|

Monday: |

Rightmove house prices (Oct, 12:01am). |

|

Tuesday: |

Public sector finances (Sept, 7am). |

|

Wednesday: |

Headline & core CPI, RPI & PPI (Sept, 7am); Land Registry house price index (Aug, 9:30am). |

|

Thursday: |

CBI industrial trends survey (Oct, 11am). |

|

Friday: |

Gfk consumer confidence (Oct, 12:01am); retail sales (Sept, 7am); S&P manufacturing & service sector PMIs (October first estimates, 9:30am). |

|

Key earnings: |

Barclays (Wed); Lloyds Banking (Thurs); NatWest Group (Fri). |

Fig D: UK S&P manufacturing & service sector PMIs

Key Asia-Pacific Macro Data & Events

Key Asia-Pacific Macro Data & Events

|

Events: |

China's Communist Party holds plenum on its 15th five-year plan (Mon to Thurs); PBOC policy decision (Mon, 2am); speech by BOJ’s Takata (Mon, 4:50am); speeches by RBA’s Jones (Tues, 12:45am), Bullock (Fri, 1:05am). |

|

Monday: |

Chinese new & used home prices (Sept, 2:30am); Chinese GDP (Q3, 3am); Chinese activity (industrial production, retail sales, fixed asset investment & unemployment rate – Sept, 3am). |

|

Tuesday: |

Japanese machine tool orders (September final estimate, 7am). |

|

Wednesday: |

Japanese imports/exports, & trade balance (Sept, 12:50am). |

|

Thursday: |

Australian S&P manufacturing & services sector PMIs (Oct first estimates, 12am). |

|

Friday: |

Japanese headline & core CPI (Sept, 12:30am); Japanese Jibun Bank manufacturing & services sector PMIs (October first estimate, 1:30am); Japanese ESRI leading index (August final estimate, 6am). |

|

Key earnings: |

BHP Group Ltd (Mon); China Telecom (Tues); Newmont DRC, Wesfarmers (Thurs); Shin-Etsu Chemical, BOC Hong Kong (Fri). |

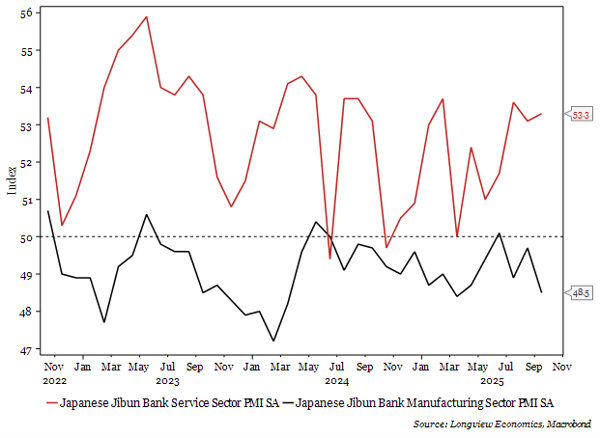

Fig E: Japanese Jibun Bank manufacturing & services sector PMIs

This Week:

Longview on Friday, 17th October 2025:

“No Smoke Without Fire”

Quant Monthly Appendix II, 15th October 2025:

Global Macro Report, 14th October 2025:

“UK: Cyclical Upswing Expected in 2026”

Longview ‘Tactical’ Alert No. 94, 13th October 2025:

“Stay ‘Tactically’ Cautious"

Daily Dose of Macro & Markets:

Daily Dose of Macro & Markets 16th October 2025:

“Chinese Housing Market – Stabilising?”

Daily Dose of Macro & Markets 15th October 2025:

“UK -> Slowing Labour Market Adds to Easing Pressures”

Daily Dose of Macro & Markets 14th October 2025:

“Another Day, Another Deal”

Last Week:

Longview on Friday, 10th October 2025:

“US –> Downside Inflation Surprise Expected In 2026”

Global Macro Report, 9th October 2025:

“UK: The Path to Lower Inflation A.k.a. ‘Top Down’ & ‘Bottom Up’ Perspectives”

Quant Monthly Appendix, 8th October 2025:

“S&P500 Sector Valuation Overview”

Daily Dose of Macro & Markets:

Daily Dose of Macro & Markets 9th October 2025:

“Fed Policy – Drifting in the Dark?”

Daily Dose of Macro & Markets 8th October 2025:

“OIL: Another Step Towards (More) Oversupply”

Daily Dose of Macro & Markets 7th October 2025:

“Gold at $4,000: (Relatively) Overpriced?”

Weekly Risk Appetite Gauge:

'Weekly Risk Appetite Gauge', 6th October 2025:

“Signs of Euphoria-> (still) Building in Global Markets”