The State of Markets: “All Eyes on the Fed & Big Tech Earnings”

A sense of calm returned to markets this week. In particular, US equities worked their way higher and volatility eased off (reversing the uptrend from the prior two weeks, see chart). Stronger than expected earnings therefore appear to have underpinned equities this week and, on today’s softer CPI print, many indices have made new highs (albeit only just).

Risks, therefore, continue to be sidelined by markets, including those around tariffs, the US government shutdown, and stress in certain pockets of the banking system. How equities close today will be watched closely. So too will the price action in gold and silver (i.e. where crowded long positioning has started to unwind).

All eyes next week will be on the Fed’s policy decision. While markets are priced for a 25bps rate cut, the tone of Powell’s press conference is also key (particularly after last month’s ‘insurance cut’). Other central bank decisions next week include the BoJ and ECB on Thursday, and the Bank of Canada on Wednesday. President Trump is also scheduled (Thursday) to meet President Xi next week to discuss the trade dispute.

With the US government shutdown ongoing, most federal data releases are likely to remain suspended. In Europe, the focus will be on Q3 GDP, with Spain reporting on Wednesday, followed by France, Italy, Germany, and the Eurozone on Thursday. It’s also ‘inflation week’ in Europe, with October flash CPI prints for Spain and Germany on Thursday, followed by France, Italy, and the Eurozone on Friday. In China, October manufacturing and services PMIs are due Friday. Meanwhile, US earnings season continues, and the key highlights include Microsoft, Alphabet, and Meta on Wednesday, and then Apple and Amazon on Thursday. Please see below for a full list of next week’s key data and events.

Key chart: VIX candlestick shown with 50, 90 & 200 day moving averages (%)

Upcoming Important Data/Events This Week:

Upcoming Important Data/Events This Week:

|

Events: |

NB The US government shutdown is ongoing – and delaying the release of certain data points. Fed policy decision (Wed, 6pm) followed by speech from Powell (6:30pm); BOJ policy decision (Thurs, 3am) followed by speech from BOJ’s Ueda (6:30am); ECB policy decision (Thurs, 1:15pm) followed by Lagarde press conference (1:45pm); Bank of Canada rate decision (Wed, 1:45pm); meeting between Xi and Trump to discuss trade dispute (on sidelines of the Apec Summit in South Korea, Thurs). |

|

Monday: |

US durable goods orders (September first estimate, 12:30pm). |

|

Tuesday: |

US Conference Board Consumer Confidence (Oct, 2pm). |

|

Wednesday: |

US pending home sales (Sept, 2pm); UK net consumer credit, mortgage approvals & M4 money supply (Sept, 9:30am). |

|

Thursday: |

N/A |

|

Friday: |

US personal income & spending including headline & core PCE (Sept, 1:30pm); Chinese Caixin manufacturing & service sector PMI (Oct, 1:30am). |

|

Key earnings: |

Visa A, United Parcel Service, PayPal, Samsung (Tues); SK Hynix Inc, Microsoft, Alphabet, Meta Platforms, Boeing (Wed); BYD Electronic, Samsung Electronics, Apple, Amazon.com, Eli Lilly, Mastercard (Thurs). |

Key Research

The SHORT VIEW (& market positioning), 20th October 2025:

“Gold: Blow-Off Top?”

There was a dramatic reversal in the gold price on Friday.

That is, after rallying ~$1,000 since August (i.e. up 30% in just two months), there was a bearish Key Day Reversal (KDR), see FIG 1. That happens when an asset price opens higher, makes a new intraday high, and then closes below the low of the prior day. Technically, it’s a bearish signal which often marks a change in the near term trend (in this case from bullish to bearish).

As is so often the case in markets, price drives opinion (when it should be the other way around). Having rallied 63% this year, the gold price is on track for its strongest year since 1979. Opinion in markets has therefore been building. Measured sentiment readings are bullish and generating a contrarian SELL signal (e.g. see the CONSENSUS Inc. indicator). Anecdotally sentiment is also strong with well-known voices calling for more upside. That includes, for example, Ray Dalio who argued last month that “gold should be 10-15% of [a well-diversified] portfolio”.

Key North American Macro Data & Events:

|

Events: |

NB The US government shutdown is ongoing – and delaying the release of certain data points. Fed policy decision (Wed, 6pm) followed by speech from Powell (6:30pm); Bank of Canada rate decision (Wed, 1:45pm); speeches by Fed’s Logan (Thurs, 5:15pm & Fri, 1:30pm), Hammack and Bostic (Fri, 4pm); meeting between Xi and Trump to discuss trade dispute (on sidelines of the Apec Summit in South Korea, Thurs). |

|

Monday: |

US durable goods orders (September first estimate, 12:30pm); US Dallas Fed manufacturing sector activity (Oct, 2:30pm). |

|

Tuesday: |

US FHFA house price index (August, 1pm); US S&P/Case-Shiller 20-city & national house prices (Aug, 1pm); US Conference Board Consumer Confidence (Oct, 2pm); US Richmond Fed manufacturing index (Oct, 2pm); US Dallas Fed service sector activity (Oct, 2:30pm). |

|

Wednesday: |

US wholesale & retail sales & inventories (Sept, 12:30pm); pending home sales (Sept, 2pm). |

|

Thursday: |

US weekly jobless claims (12:30pm). |

|

Friday: |

Canadian GDP (Aug, 1:30pm); US personal income & spending including headline & core PCE (Sept, 1:30pm); US Chicago PMI (Oct, 1:45pm). |

|

Key earnings: |

Welltower, Cadence Design, Waste Management, NXP (Mon); Visa A, UnitedHealth, NextEra Energy, American Tower, Royal Caribbean Cruises, Sherwin-Williams, Mondelez, Ecolab, United Parcel Service, Corning, PayPal, Regeneron Pharma, Electronic Arts (Tues); Microsoft, Alphabet, Meta Platforms, Caterpillar, ServiceNow Inc, Verizon, Boeing, KLA Corp, ADP, Agnico Eagle Mines, MercadoLibre, CVS Health Corp, Starbucks, Equinix, Fiserv, TE Connectivity, American Electric Power, Chipotle Mexican Grill, Public Storage, Phillips 66 (Wed); Apple, Amazon.com, Eli Lilly, Mastercard, Gilead, Stryker, S&P Global, Comcast, Altria, Southern, Trane Technologies, ICE, Bristol-Myers Squibb, Canadian Natural, Cigna, Strategy, Howmet, Motorola, Arthur J Gallagher, Republic Services, Monster Beverage, Quanta Services, L3Harris Technologies, Monolithic (Thurs); Exxon Mobil, AbbVie, Chevron, Linde PLC, Aon, Imperial Oil, Colgate-Palmolive, Dominion Energy (Fri). |

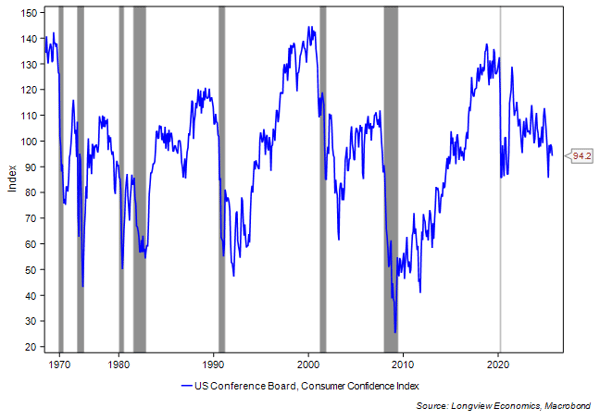

Fig B: US Conference Board consumer confidence (index)

Key European Macro Data & Events

Key European Macro Data & Events

|

Events: |

ECB policy decision (Thurs, 1:15pm) followed by Lagarde press conference (1:45pm); ECB pre rate decision quiet period (Mon to Wed). |

|

Monday: |

German IFO business climate (Oct, 9am); ECB 1 & 3 year CPI expectations (Sept, 9am); Eurozone M3 money supply (Sept, 9am); French total jobseekers (Q3, 11am). |

|

Tuesday: |

Eurozone new car registrations (Sept, 5am); German GfK consumer confidence (Nov, 7am); Italian ISTAT consumer & manufacturing confidence (Oct, 9am). |

|

Wednesday: |

Spanish GDP (Q3 first estimate, 8am); Spanish retail sales (Sept, 8am); Italian PPI (Sept, 11am). |

|

Thursday: |

GDP for France (6:30am), Italy (9am), Germany (9am) & Eurozone (10am) – all Q3 first estimates; French GDP & consumer spending (Q3 first estimate, 6:30am); headline CPI – all October first estimates for Spain (8am) & Germany (1pm); German unemployment (Oct, 8:55am); Eurozone consumer confidence (October final estimate, 10am); Eurozone unemployment rate (Sept, 10am); Italian unemployment rate (Sept, 10am); Italian industrial sales (Aug, 11am). |

|

Friday: |

Headline CPI – October first estimates for France (7:45am), Italy (10am); EZ headline & core CPI (10am); French PPI (Sept, 7:45am); German import price index (Sept, 8am); German retail sales (Sept, 8am); Spanish current account balance (Aug, 9am). |

|

Key earnings: |

Iberdrola, Air Liquide, BNP Paribas, Danone, UCB (Tues); Equinor, Airbus Group, Santander, Deutsche Bank AG, Mercedes Benz Group (Wed); Shell, Schneider Electric, TotalEnergies SE, Anheuser Busch Inbev, BBVA, AXA, ING Groep, Credit Agricole, Volkswagen VZO, Saint Gobain, Universal Music NV, Argen-X (Thurs); Intesa Sanpaolo, Caixabank (Fri). |

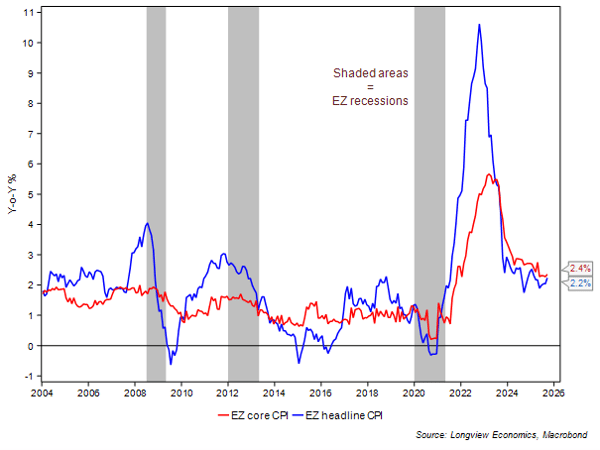

Fig C: Eurozone headline & core CPI (Y-o-Y %)

Key UK Macro Data & Events

Key UK Macro Data & Events

|

Events: |

N/A |

|

Monday: |

CBI distributive trade survey (Oct, 11am). |

|

Tuesday: |

BRC shop price index (Oct, 12:01am). |

|

Wednesday: |

Net consumer credit, mortgage approvals & M4 money supply (Sept, 9:30am). |

|

Thursday: |

N/A |

|

Friday: |

Lloyds business barometer (Oct, 12:01am); Nationwide house prices (Oct, 8am). |

|

Key earnings: |

HSBC (Tues); GSK plc (Wed). |

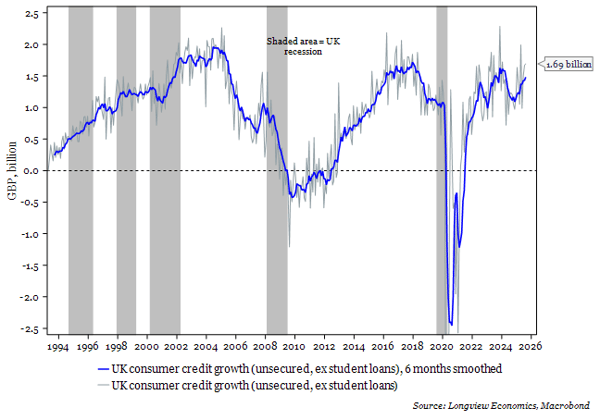

Fig D: UK consumer credit growth (billion)

Key Asia-Pacific Macro Data & Events

Key Asia-Pacific Macro Data & Events

|

Events: |

Fireside chat by RBA’s Bullock (Mon, 8:15am); BOJ policy decision (Thurs, 3am) followed by speech from BOJ’s Ueda (6:30am); meeting between Xi and Trump to discuss trade dispute (on sidelines of the Apec Summit in South Korea, Thurs). |

|

Monday: |

Chinese industrial profits (Sept, 1:30am). |

|

Tuesday: |

N/A |

|

Wednesday: |

Australian CPI (Sept & Q3, 12:30am); Japanese ESRI consumer confidence (Oct, 5am). |

|

Thursday: |

Japanese jobless rate (Sept, 11:30pm); Japanese core CPI (Oct, 11:30pm); Japanese retail sales (Sept, 11:50pm); Japanese industrial production (September first estimate, 11:50pm). |

|

Friday: |

Australian private sector credit (Sept, 12:30am); Australian PPI (Q3, 12:30am); Chinese Caixin manufacturing & service sector PMI (Oct, 1:30am); Japanese housing starts (Sept, 5am). |

|

Key earnings: |

Samsung, Advantest Corp, Jiangsu Hengrui (Tues); SK Hynix Inc, Keyence (Wed); Samsung Electronics, LG Energy Solution, Hitachi, Japan Tobacco, Agricultural Bank China, ICBC, China Construction Bank, Kweichow Moutai, China Petrol & Chemical Corp, Bank of Communications, China Citic Bank, Merck&Co, Ping An Insurance, Budweiser, BYD Electronic Int (Thurs); Tokyo Electron, KDDI Corp, Mitsubishi Electric, Hoya Cor (Fri). |

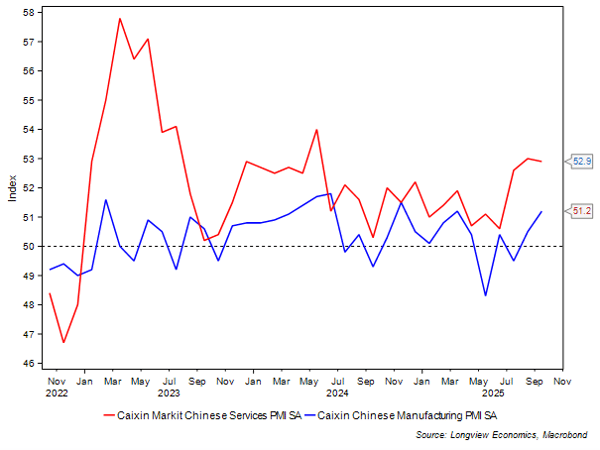

Fig E: Chinese Caixin manufacturing & service sector PMIs

This Week:

This Week:

Longview on Friday, 24th October 2025:

“S&P500 – False Breakout?”

Recommended Global Macro Trade Update, 22nd October 2025:

“Move SHORT Gold & Stay SHORT Gold vs. Silver”

The SHORT VIEW (& market positioning), 20th October 2025:

Daily Dose of Macro & Markets:

Daily Dose of Macro & Markets 23rd October 2025:

“OIL: Bear Market Ongoing”

Daily Dose of Macro & Markets 22nd October 2025:

“Reeves’ Fiscal Headache: How Big is the UK Fiscal Shortfall?”

Daily Dose of Macro & Markets 21st October 2025:

“All Eyes on China’s Fourth Plenum [& Macro Data]”

Weekly Risk Appetite Gauge:

'Weekly Risk Appetite Gauge', 20th October 2025:

“Wave Two Relief Rally – Almost Complete”

Last Week:

Longview on Friday, 17th October 2025:

Quant Monthly Appendix II, 15th October 2025:

Global Macro Report, 14th October 2025:

“UK: Cyclical Upswing Expected in 2026”

Longview ‘Tactical’ Alert No. 94, 13th October 2025:

“Stay ‘Tactically’ Cautious”

Daily Dose of Macro & Markets:

Daily Dose of Macro & Markets 16th October 2025:

“Chinese Housing Market – Stabilising?”

Daily Dose of Macro & Markets 15th October 2025:

“UK -> Slowing Labour Market Adds to Easing Pressures”

Daily Dose of Macro & Markets 14th October 2025:

“Another Day, Another Deal”