Please find below an extract from our latest SHORT VIEW - the full piece is available to private investors as part of our Macro Trader subscription. For institutional clients, please get in touch at info@longvieweconomics.com.

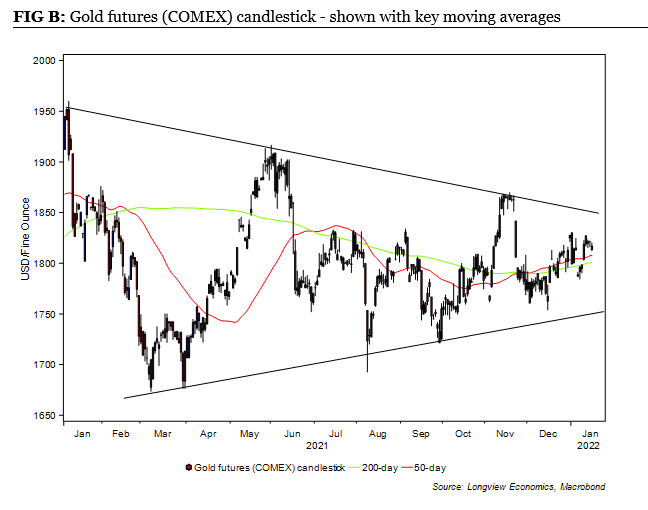

Despite heightened volatility amongst various asset classes over the past 12 months, whether interest rate futures, bond yields or base metals, the gold price has traded sideways for the past year. Indeed, on 19th January last year gold futures traded in a range of $1802.0 – $1842.9 (per ounce). Today (at time of writing) gold futures are trading at $1818.75. The behaviour of the silver price is not much different (albeit it’s approx. 6% below its level from a year ago).

Perhaps reflecting that year of sideways price action, the outlook for the gold price is the source of much disagreement: Crypto enthusiasts, and some traditional investors, believe gold’s role is being replaced (partially, or wholly) by the new digital currencies (especially bitcoin); others, including most famously Warren Buffet, continue to view it as a ‘barbarous relic’ and a wasted use of capital; while those who regard it as an inflation hedge are confused about its sideways (to modestly lower) price action over the past 18 months as consumer price inflation has been making 30 year highs around the world.

Indeed, as laid out above, the gold price has traded in a tight, and increasingly narrow range for most of the past 12 months. With that, it’s formed what technical charting analysts would refer to as a ‘pennant price pattern’. From the perspective of technical analysis, therefore, the gold price is moving towards/is close to a breakout phase (i.e. as it nears the end of the pennant).

The key question, therefore, is which way will it break (higher or lower)? & What is the fundamental and model set-up at this current time (which will drive its breakout one way or the other)?