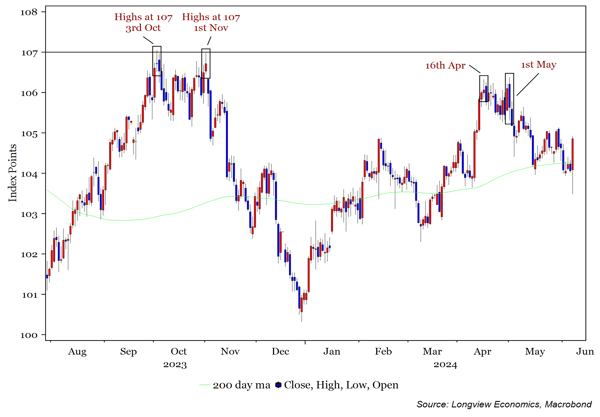

Earlier this year, in April, the dollar (DXY) rally failed before the currency made it back to its 2023 highs at 107 (see fig 1). Since then, it’s trended lower, making lower lows and lower highs. On Friday it tested its 200 day moving average and, with the help of stronger than expected macro data (NFP), found support at that level.

The key question, in the near term therefore, is: Will the dollar hold at around that key support level, and begin to work its way higher? Or will it break down/weaken further over coming weeks?

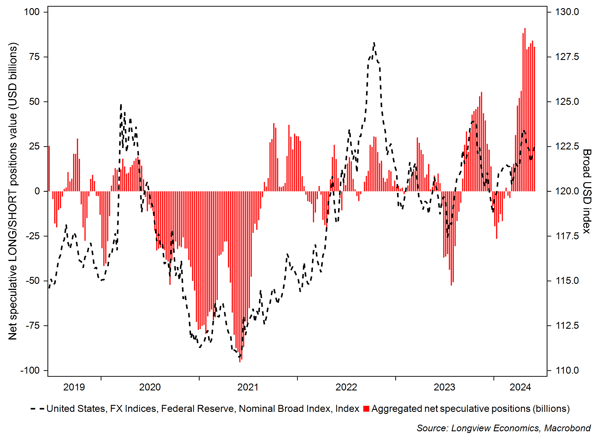

From a models’ and positioning perspective, recent dollar weakness is likely to persist. Most notably, net LONG positioning remains relatively crowded (see fig 2); measured sentiment readings are bullish (a contrarian sell signal for the dollar) while a number of Longview technical indicators have recently been on/close to SELL.

Furthermore, there’s some evidence that the US economy is entering a growth ‘soft patch’. GDP data, for example, has recently been soft (and has been revised lower), some of last week’s ISM manufacturing and services data was soft, while leading indicators of the labour market have rolled over (and point to weaker hiring activity in coming months).

A key risk, therefore, is that (some) Fed cuts are priced back into the rates market and, with that, US Treasury yields move lower. That, if it happened, would put downward pressure on the dollar, especially given the current positioning and sentiment set-up. Either way, the 200 day moving average is a key level to watch. We’ll be analysing this further in this weeks’ forthcoming SHORTview publication (available for subscribers).

Fig 1: Aggregated* USD value of positioning vs. Broad US dollar index

Fig 2: Aggregated* USD value of positioning vs. Broad US dollar index

*Aggregated positioning across major USD currency pairs.