SUMMARY OF MARKETS LAST WEEK:

The Philly SOX (up 32% in 2024) was approx. 1% lower over the course of the week (see chart). Nvidia, which has been the key leadership stock in the US this year, was down 4%; while others, like Broadcom (down ~4%), were also lower. Both those stocks, earlier this month, were already notably overextended to the upside (hence due some giveback). Elsewhere the European political situation took a back seat (as the EZ govvie bond spreads eased modestly over the past handful of trading sessions). Round one of the French elections, though, are due next weekend (so spreads will remain a focus).

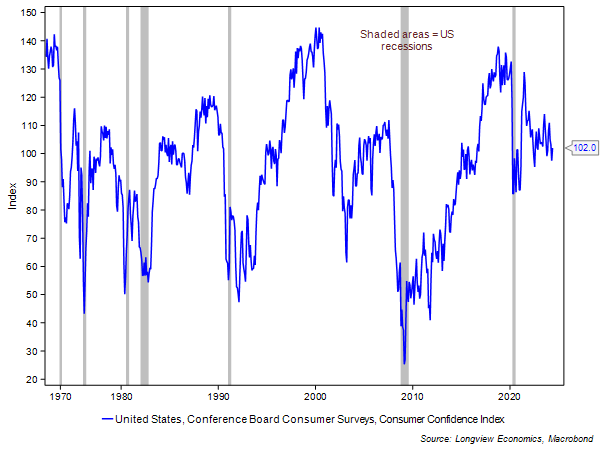

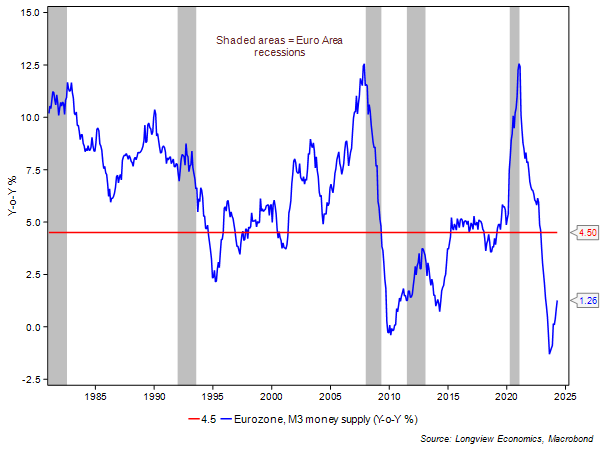

Other key focuses of the market next week will include various pieces of US macro data (Conference Board consumer confidence on Tuesday; US durable goods orders on Thursday; & Chicago PMI on Friday). Last month’s Chicago PMI reading was exceptionally weak (35.4). Consensus is that the index will bounce to 40.0. German IFO is always key (Monday) – the ‘expectations less current conditions’ index has been rallying sharply (and typically leads phases of EZ economic re-acceleration); while Sweden holds a monetary policy meeting on Thursday (NB last month the central bank cut the policy rate by 25bps to 3.75%).

Our short-term view on equity market direction, as always, is laid out in our ‘Daily Risk Appetite Gauge’ publication (with ‘1 – 2’ week recommendations on S&P500 futures). Our medium term (‘1 – 4’ month view) is addressed in our monthly ‘Tactical Asset Allocation’ publication. This was last updated earlier this month. Longer term investors should refer to the ‘Strategic Global Asset Allocation’ reports (for our ‘6 months to 2 years’ recommended global asset allocation portfolio).

Key chart: Philly SOX semiconductor index shown with 50 day moving average

The most important macro data, events & earnings reports out next week

|

Events: |

Riksbank policy decision (Thurs, 8:30am); Bank of England publishes financial stability report and FPC summary (Thurs, 10am). |

|

Monday: |

German IFO business climate (Jun, 9am). |

|

Tuesday: |

US Conference Board consumer confidence (Jun, 3pm). |

|

Wednesday: |

US new home sales (May, 3pm). |

|

Thursday: |

Eurozone M3 money supply including monthly loans to households and corporates (May, 9am); US durable goods orders (May first estimate, 1:30pm). |

|

Friday: |

French headline CPI (June first estimate, 7:45am); US personal income & spending including headline & core PCE inflation (May, 1:30pm); US Chicago PMI (Jun, 2:45pm). |

|

Key earnings: |

FedEx (Tues); Micron (Wed); Nike, H&M (Thurs). |

Key Longview research published last week

You'll find some extracts from research we've published recently below. The full reports are available to subscribers. To see the options we have available for individual investors, please click here.

Quarterly Asset Allocation No. 58, 20th June 2024:

“How Magnificent Are The ‘MAG7’?”

The valuation gap between US asset prices (specifically equities) and most of the rest remains stretched.

In the US, the equity market is expensive. Its forward PE multiple is 20.8x consensus earnings expectations; its equity risk premium is at one of its lowest levels on record (only more expensive in the TMT bubble – fig 9di); the US Shiller PE ratio is above its 1929 peak (fig 9i); while 8 of the 11 S&P500 GICS level 1 sectors are trading above their 80th or 90th highest percentiles of their entire PE ratio history (i.e. back to the 1980s). Consistent with that, Longview’s proprietary valuation model is on strong SELL (although has been on SELL since early 2023 – fig 9viii).

North America: Key events next week

|

Events: |

Speeches by the Fed’s Daly on the Economy and monetary policy (Mon, 7pm), Cook at the Economic Club of New York (Tues, 5pm), Bowman in Q&A (Tues, 7:15pm) & Barkin at the Global Interdependence Center’s conference (Fri, 11am). |

|

Monday: |

US Dallas Fed manufacturing activity (Jun, 3:30pm). |

|

Tuesday: |

US Philadelphia Fed service sector activity (Jun, 1:30pm); US Chicago Fed national activity (May, 1:30pm); Canadian headline & core CPI (May, 1:30pm); US FHFA house price index (Apr, 2pm); US S&P/Case-Shiller 20-city & national house prices (Apr, 2pm); US Conference Board consumer confidence (Jun, 3pm); US Richmond Fed manufacturing & business conditions (Jun, 3pm); US Dallas Fed services activity (Jun, 3:30pm). |

|

Wednesday: |

US new home sales (May, 3pm). |

|

Thursday: |

Canadian CFIB business barometer (Jun, 12pm); Canadian SEPH payroll employment change (Apr, 1:30pm); US GDP (Q1 third estimate & May, 1:30pm); US weekly jobless claims (1:30pm); US durable goods orders (May first estimate, 1:30pm); US pending home sales (May, 3pm); US Kansas City Fed manufacturing activity (Jun, 4pm). |

|

Friday: |

Canadian monthly GDP (Apr, 1:30pm); US personal income & spending including headline & core PCE inflation (May, 1:30pm); US Chicago PMI (Jun, 2:45pm); US Michigan sentiment (June final estimate, 3pm); US Kansas City Fed services activity (Jun, 4pm). |

|

Key earnings: |

FedEx (Tues); Micron, Paychex (Wed); Nike (Thurs). |

Fig B: US Conference Board consumer confidence (index)

Eurozone: Key events next week

|

Events: |

Speeches by the ECB’s Villeroy in Paris (Mon, 1:30pm), Schnabel in Berlin (Mon, 4:30pm), Stournaras in Athens (Tues, 10am), Rehn, Panetta & Lane on monetary policy in low and high inflation environments (Wed, 10:30am – 11:40am), Kazaks in Helsinki (Wed, 12:45pm) & Villeroy in Paris (Fri, 11am); Riksbank policy decision (Thurs, 8:30am). |

|

Monday: |

German IFO business climate (Jun, 9am). |

|

Tuesday: |

N/A |

|

Wednesday: |

German GfK consumer confidence (Jul, 7am); French INSEE consumer confidence (Jun, 7:45am). |

|

Thursday: |

Italian ISTAT consumer & manufacturing confidence (Jun, 9am); Eurozone M3 money supply including monthly loans to households and corporates (May, 9am); Eurozone consumer confidence (June final estimate, 10am); Italian PPI (May, 10am). |

|

Friday: |

German import prices & retail sales (May, 7am); French consumer spending (May, 7:45am); French headline CPI (June first estimate, 7:45am); French headline PPI (May first estimate, 7:45am); German unemployment change (Jun, 8:55am); ECB 1 & 3 year inflation expectations (May, 9am); Italian industrial sales (Apr, 9am); Italian headline CPI (June first estimate, 10am). |

|

Key earnings: |

H&M (Thurs). |

Fig C: Eurozone M3 money supply (Y-o-Y %)

UK: Key events next week

|

Events: |

Bank of England publishes financial stability report and FPC summary (Thurs, 10am). |

|

Monday: |

CBI industrial trends orders (Jun, 11am). |

|

Tuesday: |

N/A |

|

Wednesday: |

CBI distributive trade survey (Jun, 11am). |

|

Thursday: |

N/A |

|

Friday: |

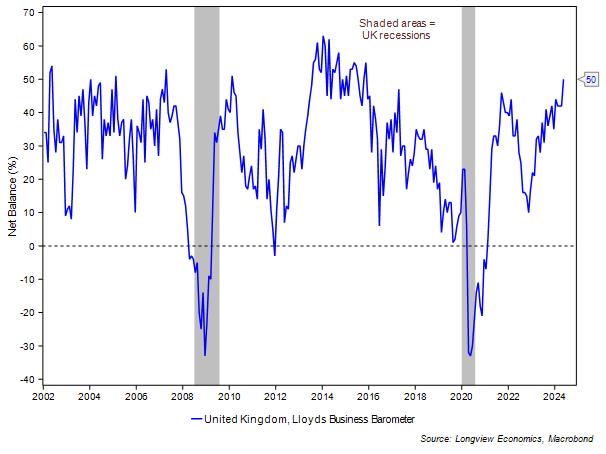

Lloyds business barometer (Jun, 12:01am); GDP (Q1 final estimate, 7am) & Q1 current account balance. |

|

Key earnings: |

N/A |

Fig D: UK Lloyds business barometer (net balance %)

Asia-Pacific: Key events next week

|

Events: |

BOJ releases summary of opinions for June policy meeting (Mon, 12:50am); speeches by the RBA’s Kent at the ABA Banking conference (Wed, 12:35am) & Hauser at the A50 Australian Economic forum (Thurs, 11am); market holiday in New Zealand on account of New Year’s Day (Fri). |

|

Monday: |

N/A |

|

Tuesday: |

Japanese PPI services (May, 12:50am); Australian Westpac consumer confidence (Jun, 1:30pm); Japanese ESRI leading index (April final estimate, 6am). |

|

Wednesday: |

Australian Westpac leading index (May, 1:30pm); Australian headline CPI (May, 2:30am). |

|

Thursday: |

Japanese retail sales (May, 12:50am); Australian consumer inflation expectation (Jun, 2am); Chinese industrial profits (May, 2:30am); Australian job vacancies (May, 2:30am). |

|

Friday: |

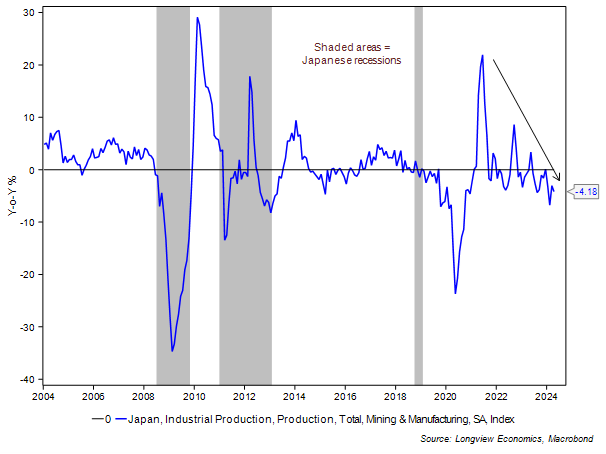

Japanese jobless rate (May, 12:30am); Japanese industrial production (May first estimate, 12:50am); Australian private sector credit (May, 2:30am); Japanese housing starts (May, 6am). |

|

Key earnings: |

N/A |

Fig E: Japanese industrial production (Y-o-Y %)

Longview research published recently

Last week:

Longview on Friday, 21st June 2024:

“Is a Currency Crisis (& Secular Dollar Bear Market) Brewing?”

Quarterly Asset Allocation No. 58, 20th June 2024:

“How Magnificent Are the ‘MAG7’?”

Quarterly Asset Allocation No. 58, 17th June 2024:

“US Expansion Likely Ongoing (Recession Risk = 20%)”

Prior week:

Longview on Friday, 14th June 2024:

“Brewing Shift in the Shape of Global Growth”

Quarterly Asset Allocation No. 58, 12th June 2024:

“China: ‘Pushing on a String’”