|

Events:

|

Speeches by the Fed’s Harker on the economic outlook (Mon, 6pm), Cook gives acceptance remarks (Tues, 2am), Barkin on the US economy (Tues, 3pm), Collins gives keynote address (Tues, 4:40pm), Logan in Q&A (Tues, 6pm), Kugler & Musalem on the economy and monetary policy (Tues, 6pm & 6:20pm), Goolsbee in panel discussion (Tues, 7pm) & Barkin on the economic outlook (Thurs, 9pm); US bank holiday (Wed).

|

|

Monday:

|

Canadian housing starts (May, 1:15pm); US Empire manufacturing (Jun, 1:30pm); Canadian existing home sales (May, 2pm).

|

|

Tuesday:

|

US New York Fed services business activity (Jun, 1:30pm); US retail sales (May, 1:30pm); US industrial & manufacturing production & capacity utilisation (May, 2:15pm); US business inventories (Apr, 3pm); US total net TIC flows (Apr, 9pm).

|

|

Wednesday:

|

US NAHB homebuilders index (Jun, 3pm).

|

|

Thursday:

|

US current account balance (Q1, 1:30pm); US weekly jobless claims (1:30pm); US housing starts & building permits (May, 1:30pm); US Philadelphia Fed business outlook (Jun, 1:30pm).

|

|

Friday:

|

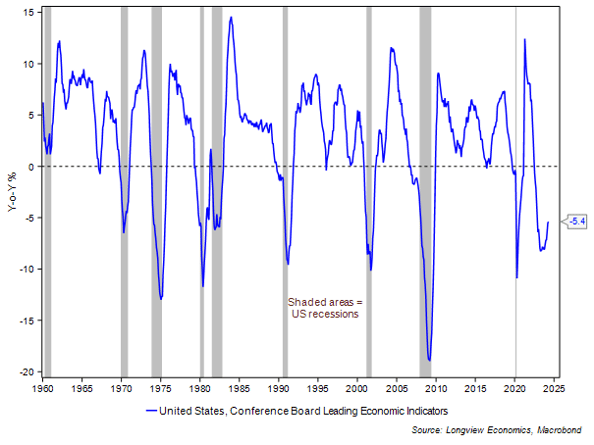

Canadian retail sales (Apr, 1:30pm); US S&P manufacturing & service sector PMIs (June first estimates, 2:45pm); US Conference Board leading index (May, 3pm); US existing home sales (May, 3pm).

|

|

Key earnings:

|

Lennar (Mon); Accenture, Kroger (Thurs).

|

Fig B: US Conference Board leading index (Y-o-Y %)

|