Oil prices have formed a pennant pattern in the past 12 months. That is, since topping in September last year, they have been making lower highs; as well as higher lows since last December. The second major high (April 2024), for example, was on the Israel/Iran conflict, while the second major low (early June) was on news that ‘OPEC+’ would begin to reverse its voluntary production cuts (starting Q4). Currently, therefore, with an 8.8% pullback since early July, oil is trading ~3% above the bottom of its pennant pattern (i.e. it’s next key support level).

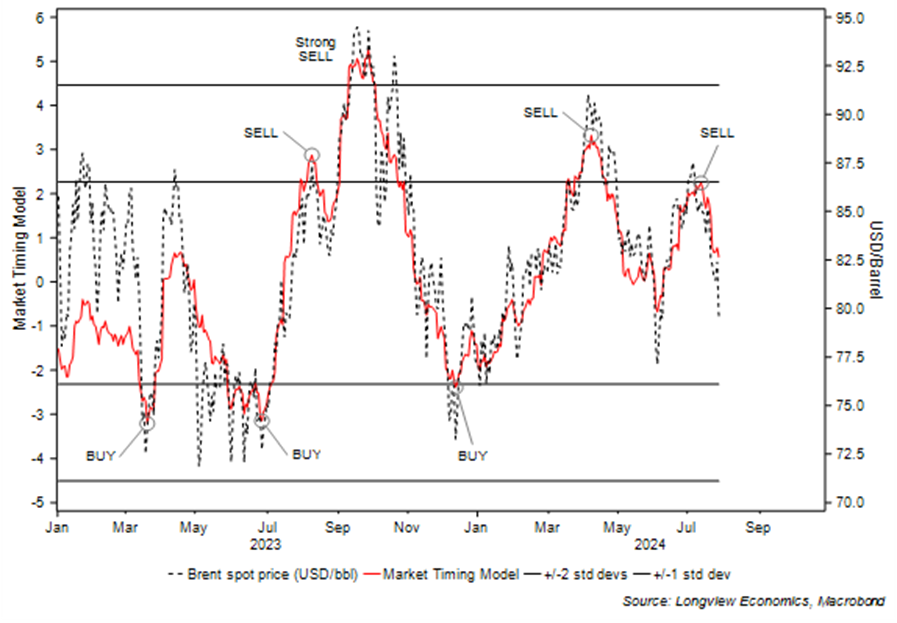

Of interest, in that respect, some models point to further downside in oil prices (and, at a minimum, a test of that level). Sentiment, for example, remains bullish (and close to generating a contrarian SELL signal), while our ‘market timing model’ for oil highlights the potential for further downside (see fig 1a).

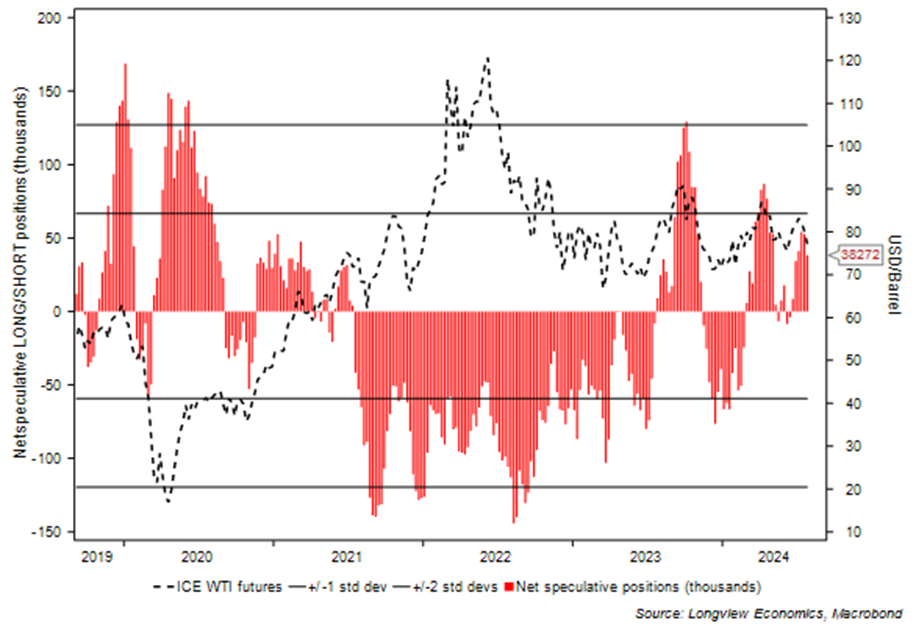

Against that, though, net LONG positions have fallen to relatively low levels (fig 1d). There’s not, therefore, much fuel for further weakness in oil prices (on that measure). In a similar vein, with Brent prices down sharply in the past five trading days, implied oil volatility (OMX) has spiked (and is now technically overextended to the upside). Some degree of fear and panic has therefore been priced into the oil market. All of which suggests that the oil price should begin to stabilise in the near term.

As such, given those mixed signals, the key question is: Will oil prices find support at the bottom of the pennant pattern? Or, will that level be broken? Answers may come later this week – with the upcoming OPEC+ Joint Ministerial Monitoring Committee meeting (August 1st).

Fig 1: Brent oil futures, shown with 50 & 200 day moving averages (US$/barrel)

Fig 1a: Brent oil market timing model vs. oil price (US$/barrel)

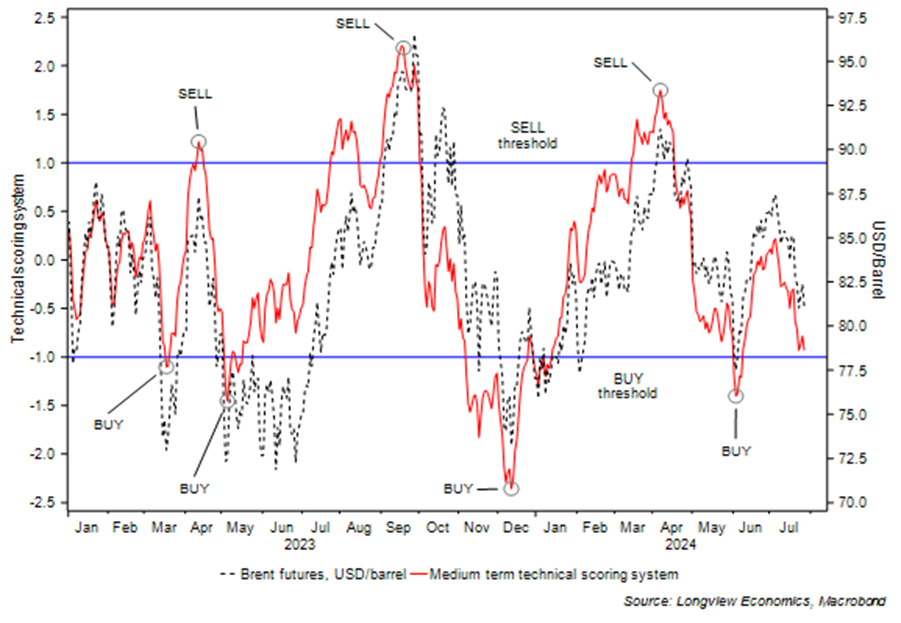

Fig 1b: Medium term technical scoring system vs. oil price (US$/barrel)

Fig 1c: Brent oil net speculative LONG/SHORT positions vs. oil price (US$/barrel)

If you have any questions on the above, or any feedback, please don't hesitate to get in contact with us either via the website, or email us at: info@longvieweconomics.com

Kind Regards

Longview Economics