Please find below a summary of the CFTC Commitment of Traders report for this week. The data represents the positions as of last Tuesday's close, published on Friday. You can find below a link to our market positioning dashboard - an interactive tool to explore the current speculative positioning of over 40 key assets. In addition, we've highlighted some interesting charts below.

This dashboard and chart bank provide the basis for our Short View publication. In the 'Short View' we analyse short term movements of key asset classes (equities, bonds, rates, currencies, commodities and volatility), principally by assessing shifts in positioning and sentiment.

The Short View, along with our Macro Trade Recommendations, are available to subscribers of our 'Macro Trader' package. For more details, or to take a 30-day free trial, check out our website!

Wheat:

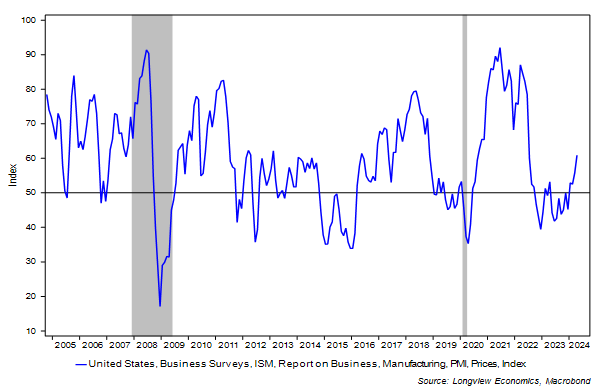

Concerns about sticky inflation in the West have risen in recent months. In particular, as well as strong monthly service sector CPI readings, various forward looking indicators point to a pick-up in inflation. The NFIB pricing plans survey, for example, has moved higher in recent months, while the ISM manufacturing & service sector ‘prices paid’ indices have also bounced (e.g. fig 3).

Food prices are also higher. In particular, wheat prices have risen to the highest level in over 6 months while corn prices are approaching YTD highs.

The key question, therefore, is: Will wheat/food prices continue rising? Or is this rally likely to fade? In other words, will food prices be inflationary or deflationary?

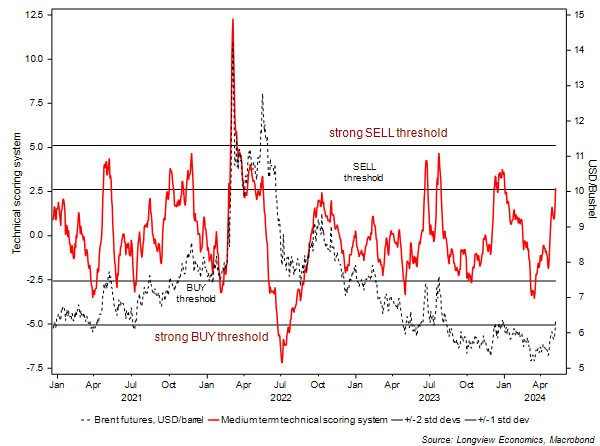

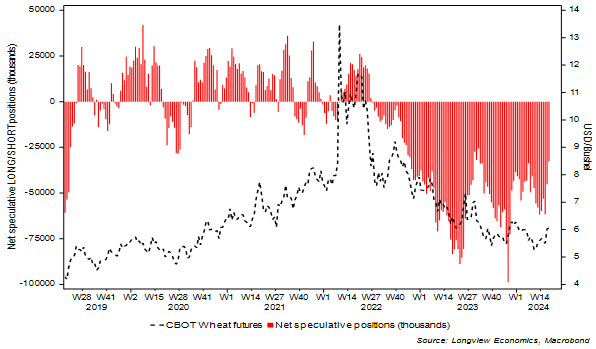

The message of our wheat price models, in that respect, is mixed. Our medium term technical scoring system, for example, is now on SELL (suggesting that wheat prices are overextended to the upside, see fig 4). Sentiment, though, remains broadly bearish, and speculators are net SHORT wheat futures (despite having reduced SHORT positioning significantly in recent weeks, see fig 1).

As such, the direction of wheat prices likely depends on the outlook for underlying supply and demand fundamentals. In that respect, upside price risks are growing. The US Department of Agriculture, for example, recently estimated lower grain exports from Ukraine this year given that farmers are switching to (more profitable) oilseeds (see HERE), US farmers are reportedly reducing their wheat acreage this year (see HERE), while the US Department of Agriculture revised up their global wheat demand forecast for a sixth consecutive month in April (see HERE).

Fig 1: Net speculative positioning (no. of contracts) vs. wheat price (USD/bushel)

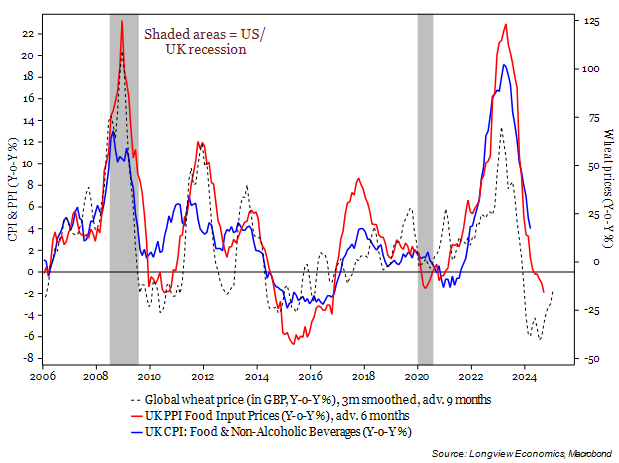

Fig 2: Wheat price & UK Food PPI (adv. 9m & 6m) vs. UK Food CPI (Y-o-Y %)

Fig 3: ISM manufacturing ‘prices paid’

Fig 4: Longview medium term technical scoring system vs. wheat prices (USD/bushel)