Conference Rules of Thumb: Short the Consensus

“Crypto is the next internet, no investors want to miss it”Source: Bloomberg - Mike Novogratz, Founder & CEO, Galaxy Digital, September 2021

“Crypto is essentially an economic cult that taps into very base human instincts of fear, greed and tribalism.”Source: Stephen Diehl, a crypto-sceptic software engineer FT

The ‘rule of thumb’ at conferences is that the consensus is almost always wrong. That is, whatever the consensus is keenest to buy, or whichever is the most widely attended session of the conference, then it usually pays to do the opposite (i.e. short that investment as it’s a crowded trade).

Last Thursday we chaired a day of sessions at an FX conference in London (an in-person and virtual ‘hybrid’ event). Of the eleven sessions we chaired, including moderating the initial two global macro panels, by far the most widely attended one was the afternoon session on cryptos. The room was packed, there wasn’t a single spare seat – in contrast to all other 10 sessions on the day (including the sparsely attended ‘central bank digital currency (CBDC)’ session which followed immediately after the one on cryptos).

That, of course, raises the question: Have we missed something on Cryptos? Are they, as Mike Novogratz (one of the cheerleaders) suggests in the quote above, ‘the next internet’? Is Bitcoin, for example, the Napster of music (i.e. the early streaming version of what is now effectively Spotify/Apple music and so on). Or is it the Netscape of web browsers (or even earlier browsers, like WorldWideWeb, launched in 199o)? Increasingly, companies and countries are adopting digital currencies into their product offerings or into their country’s legal and regulatory frameworks. El Salvador has last week, for example, become the world’s first country to adopt Bitcoin as legal tender (e.g. REUTERS) - although many are questioning the real motives of the country’s leader in adopting the crypto). Elsewhere last week, Ukraine became “the latest country to legalize bitcoin as the cryptocurrency slowly goes global” (see CNBC), while various companies continue to increase their crypto related product offerings. Fidelity, for example, has built up a wide offering of crypto related products.

Or is our original thesis correct? That is, whilst an initially intriguing idea, cryptos have, more recently, morphed into purely speculative assets.

The Original Idea

The first crypto currency (Bitcoin, BTC) was conceived in 2009 as a response to governments and central banks’ willingness to print money and debase their own currencies. By creating a currency with only a finite supply (i.e. 21 million Bitcoins) it was hoped that it would replace fiat currencies and become the currency of choice. After all, the US in its ‘free banking era’ (which lasted between 1837 and 1866) had an estimated 8,000 different types of money by 1860 (Wikipedia).

With finite supply, therefore, digital currencies should hold their value (unlike the dollar whose purchasing power is down over 90% from its level 100 years ago, i.e. after adjusting for inflation). Indeed, in many ways there are parallels with prior international monetary systems, like the hard gold standard, where increasing the amount of currency in circulation was not possible – unless there was a major discovery of new gold (i.e. given each dollar was backed by actual physical gold).

In that sense BTC, if ever widely adopted, would create a monetary system which had an anchor (i.e. a limited supply of BTCs). That would then address the issues of financial market speculation, excess liquidity creation and the associated income and wealth inequality which results from the current international dollar fiat monetary system (with its unlimited money creation, and lack of an anchor).

Speculative Asset or Germination of a New Financial System?

“He (Isaac Newton) is claimed to have said ‘[he could] calculate the motions of the heavenly bodies, but not the madness of people”Source: “Newton's financial misadventures in the South Sea Bubble"Published by Journal of the History of Science, Andrew Odlyzko, 29 August 2018“Who controls the food supply controls the people; who controls the energy can control whole continents; who controls money can control the world”Source: US Secretary of State, Henry Kissinger, 1974

In its original form, therefore, the idea is compelling.

That original form, though, has been significantly distorted in various ways.

Firstly today, there are now between 4,000 and 8,000 separate cryptocurrencies, depending on which source is correct. According to ‘CoinMarketCap’, there are 7,812 individual cryptos; according to ‘Coinlore’ its 6,241, while ‘Statista’ places the total at 5,840 and ‘Investopedia’ suggests its more than 4,000 as at January 2021.

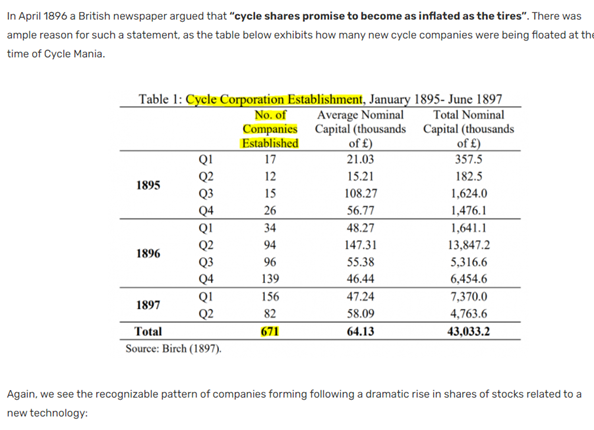

In other words, as with all financial bubbles, the rapid rise in the price attracts a fast expansion of supply. That was the case, for example, in the Chinese housing bubble post the GFC (ghost cities, for example). It was also evident in the TMT bubble (e.g. companies whose share prices got bid up simply because they had ‘technology’ in their name); or further back in history, the British bicycle company bubble in the late 1800s. The excitement surrounding the mass manufacture and adoption of bicycles at that time led to the rapid growth in the supply of new bicycle companies (table 1 below).

Table 1: UK Bicycle Companies newly formed per annum: 1895 - 1897

Source: J Catherwood, Speculation & Innovation, August 9th 2020 INVESTORAMNESIA

Clearly in the case of Cryptos, that supply response has occurred (with between 4,000 – 7,500 coins now in existence).

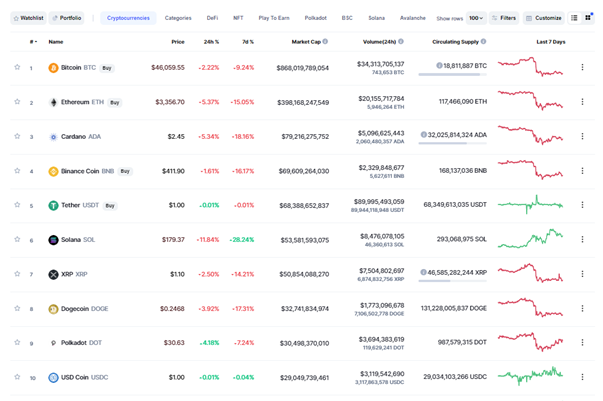

With that rapid growth in supply of Cryptos (and the pick-up in their prices), the aggregate market cap of all the outstanding coins is now over US$2 trillion. The largest, by far, is Bitcoin with a market cap of $868 billion. That’s followed by Ethereum ($398 billion), and various others – see below. By the 1,000th largest crypto (in size order), the market cap is a mere $9 million (i.e. AMLT).

FIG 1: Top 10 Crypto currencies by market capitalisation (US$)

Secondly, its ability to function as a currency is questionable.

Secondly, its ability to function as a currency is questionable.

Economists view currencies as having three roles, succinctly summarised from this St Louis Federal Reserve blog:

- “First: Money is a store of value. If I work today and earn 25 dollars, I can hold on to the money before I spend it because it will hold its value until tomorrow, next week, or even next year. In fact, holding money is a more effective way of storing value than holding other items of value such as corn, which might rot. Although it is an efficient store of value, money is not a perfect store of value. Inflation slowly erodes the purchasing power of money over time.

- Second: Money is a unit of account. You can think of money as a yardstick-the device we use to measure value in economic transactions. If you are shopping for a new computer, the price could be quoted in terms of t-shirts, bicycles, or corn. So, for instance, your new computer might cost you 100 to 150 bushels of corn at today's prices, but you would find it most helpful if the price were set in terms of money because it is a common measure of value across the economy.

Currently, Bitcoin is not a ‘medium of exchange’ – the vast majority of shops/restaurants, places to purchase goods and services do not take Bitcoin as payment. It’s not a reliable ‘store of value’, because it’s not known if it will hold its value from one day to the next. Finally, it’s not currently a ‘unit of account’ since most prices are not quoted in Bitcoin. Potentially factors two and three above (in quote) could change but realistically only if it becomes legal tender, which is unlikely in most advanced economies (see below).

Thirdly, cryptos have increasingly become a leveraged asset class and are potentially (given their unregulated nature) an area of the financial system populated with fraud.

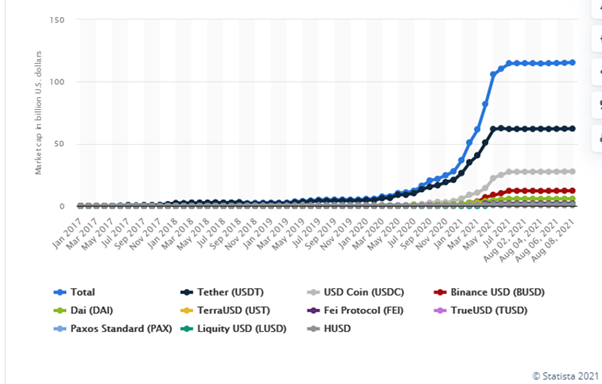

‘Stablecoins’ are a case in point. These are crypto coins which are linked to (and purportedly wholly backed by) an asset (mostly dollar denominated and typically US T-bills or equivalent). The largest and best-known stable coin is ‘Tether’, with a market cap of $68 billion. Next largest is USD Coin ($29bn), and then Binance USD ($12bn) – see chart below. According to crypto websites, Tether’s daily volume is typically larger than its market cap (i.e. daily volume of ~$100 billion or so).

FIG 2: Stablecoins’ market cap (US$bn)

There’s much debate, though, as to whether Tether’s assets are really wholly backed by US dollar assets (NB which underpins its 1 – 1 value with the USD). In other words, have the operators of Tether ‘printed’ Tethers? If they have, then there’s a risk of a ‘run on the coin’, akin to a bank run except that: i) there’s no central bank as a liquidity provider of last resort; & ii) there’s no indirect government backing for the currency (i.e. via the government’s revenue raising powers).

There’s much debate, though, as to whether Tether’s assets are really wholly backed by US dollar assets (NB which underpins its 1 – 1 value with the USD). In other words, have the operators of Tether ‘printed’ Tethers? If they have, then there’s a risk of a ‘run on the coin’, akin to a bank run except that: i) there’s no central bank as a liquidity provider of last resort; & ii) there’s no indirect government backing for the currency (i.e. via the government’s revenue raising powers).

Added to that,

“USDT tokens are involved in half of worldwide Bitcoin trades. And there have been questions about whether movements in Tether have created price manipulation in Bitcoin. One academic study(ED: see abstract below) found that…” – see quote below.“Abstract: This paper investigates whether Tether, a digital currency pegged to the U.S. dollar, influenced Bitcoin and other cryptocurrency prices during the 2017 boom. Using algorithms to analyze blockchain data, we find that purchases with Tether are timed following market downturns and result in sizable increases in Bitcoin prices. The flow is attributable to one entity, clusters below round prices, induces asymmetric autocorrelations in Bitcoin, and suggests insufficient Tether reserves before month-ends. Rather than demand from cash investors, these patterns are most consistent with the supply-based hypothesis of unbacked digital money inflating cryptocurrency prices.”Source: “Is Bitcoin Really Un-Tethered?” Original, 25 Jun 2018; Last revised: 5 Nov 2019, authored by John M. Griffin, University of Texas at Austin & Amin Shams, Ohio State University, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3195066

Whilst it’s difficult to be definitive about the evidence of fraud, the ingredients are clearly present.

As Kindleberger reminds us, all financial bubbles are built on four factors: i) a good narrative; ii) cheap money; iii) leverage and debt; & iv) rich valuations.

In this instance and given that Bitcoin is unlikely to become a currency (see above and below), it’s not clear what purpose it will serve (in which case it’s expensive). Some are suggesting it’s going to become the new digital version of gold. If adoption is widespread enough, this is possible (i.e. self-fulfilling). Unlike gold, though, there are no other possible uses. That is, gold is used in jewellery, and it has some industrial uses. If cryptos don’t become a store of value (and in our opinion won’t become a currency), then they have no use (other than as a collectible). In which case they are effectively almost worthless.

Will governments allow cryptos to operate as legal currencies? More importantly, and as Kissinger alludes to in the quote at the top of the page, governments are reticent to relinquish control of the money supply. In de Gaulle’s words, the US’s dollar hegemony is an ‘exorbitant privilege’, by which the country is able to fund almost continual current account deficits (i.e. borrow from the rest of the world). That’s been ongoing since the start of this current fiat dollar international monetary system (1971). That borrowing has facilitated/paid for the US’s wars in recent decades, facilitated US overconsumption and contributed to America’s ‘Exceptionalism’. That is, by technically ‘living beyond its means’, the US has been able to project geopolitical power, engineer strong economic recoveries, aggressively stimulate its economy (when needed), and at the same time not be concerned about paying back the debt. In an anchored monetary system, this is not possible (i.e. it’s not feasible to run persistent current account deficits with a monetary anchor and its associated liquidity restrictions).

Added to that, the global trading and financial system is dollar based (a further projection of America’s hegemonic power). Through that system the US regularly implements financial sanctions on countries that challenge it (e.g. Iran and some of its key leaders – see HERE). If the US government didn’t control the currency at the heart of that international financial system, it wouldn’t be able to exercise that power (thereby undermining its global influence). That is clearly not a choice the US government is going to make. In that sense it’s not going to allow (non CBDC) private ‘crypto’ currencies to play a meaningful role as a genuine currency in the US, nor indeed, global financial system. As Kissinger says: “He who controls the money, can control the world”.

So, while it’s possible to understand how the blockchain technology will, and does, have multiple applications which will/are widely adopted, it’s not obvious that there is a long-term role for cryptocurrencies. That, and the other classic bubble-like characteristics highlight that Bitcoin (and its sister crypto currencies) share parallels with the ‘Tulip mania’ in the 1600s (or the South Sea Bubble – see Isaac Newton quote above). ‘Tulip mania’ was about ‘tulip’ bulbs. A common plant today, but one which was only introduced into Europe in the late 1500s/1600s (and considered a luxury). At the time, tulip bulbs were changing hands for the cost of a house (with speculators famously re-mortgaging their houses to buy the bulbs). Today, of course, tulips are as good as worthless when compared to a house.

So, coming back to the original question posed in the title: Is Crypto the next subprime? It’s difficult to know with any certainty. Subprime, at the time, and as Bernanke labelled it was too small (approx. $2 trillion) and therefore supposedly easily 'contained'. Equally, though, and as per Fidelity's annual crypto survey of institutions, over 50% are already involved in the space in some way. So, while it’s not clear if crypto will infect the financial system anything like to the same extent as subprime and housing, it’s also increasingly a popular area in which companies (and individuals) are investing. Perhaps in that sense, a closer parallel is the influence of tech stocks (and quick wealth effects) in driving retail sales higher in 1999.

For now, though, money remains loose and speculative behaviour widespread. Equally the Fed seems in no hurry to accelerate the removal of monetary accommodation (probably preferring to taper very slowly). Once it does eventually get going, though, it's likely that BTC (as a highly speculative instrument) will be one of the first assets to illustrate that tightness and, in that sense, while maybe not the next subprime, cryptos should in the very least be the canary in the coalmine of the next crisis (which as we argued last week is ‘not now but is brewing’).