Summary

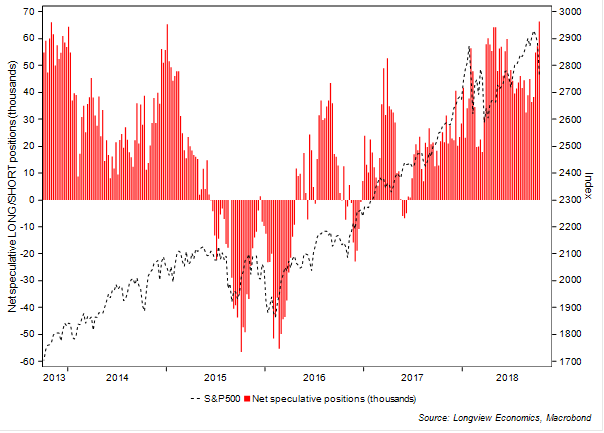

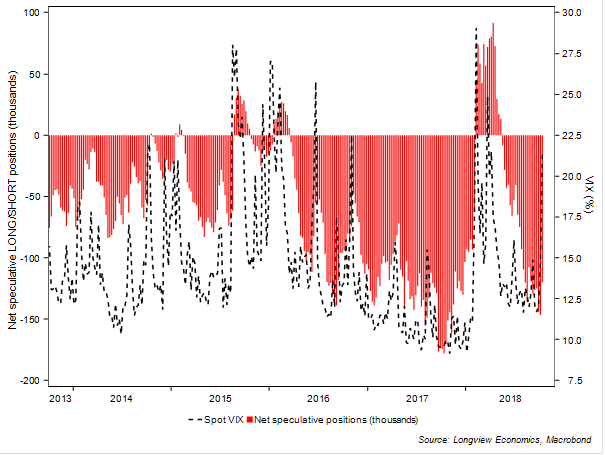

Market participants were positioned poorly for last week’s wave of risk aversion (NB positioning data is collected on Tuesday evenings, i.e. prior to the sharpest part of the global equity decline which began on Wednesday). Net LONG positioning in S&P500 futures, for example, was at its highest level since 2013, and one of its highest in this cyclical bull market (FIG A), while net LONG contracts in the DJIA were also high. Similarly, speculators were positioned for ‘risk-on’ in a number of other assets: aggregate net SHORT positioning in US Treasuries, for example, was, and remains, extreme (albeit it reduced modestly last week); net SHORT positioning in the JPY has increased further and is at high levels (fig 12); and net SHORT VIX positioning is elevated (FIG D). We remain concerned about the performance of equity markets in the near term due to a number of other factors, and expect weakness in risk assets to persist* (for more detail see LV on Friday, 12th Oct 2018: "Equities: After that, What's Next?").

FIG A: S&P500 vs. net speculative LONG/SHORT consolidated** positions

*i.e. after a near term ‘wave 2’ relief rally

**Consolidated positions aggregate the standard and mini size futures contracts (and weight the mini contracts accordingly).

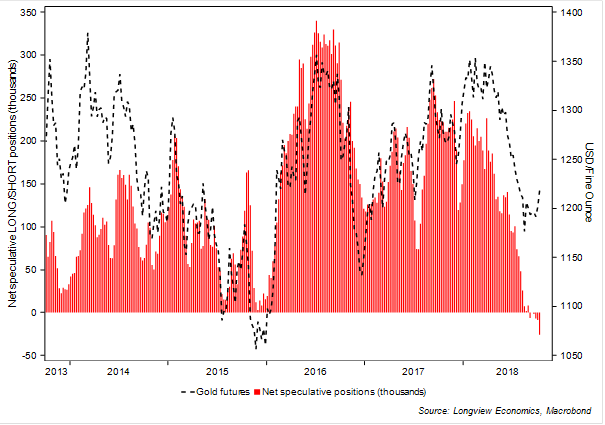

Precious metals strengthened last week following the recent phase of risk aversion. That reflected both their safe haven, defensive status as well as their net positioning. Net positioning in gold, for example (FIG B), was at its most SHORT since 2001 while speculators remain bearish on the other precious metals. Following the low in gold in August, we recommended starting to build LONG positions in gold futures on the basis of positioning as well as fundamentals (for more detail see Macro Trade No. 92, 21st Aug 2018: “Gold: Close SHORT position – Start BUILDing LONG exposure”).

FIG B: Gold futures vs. net LONG/SHORT positions

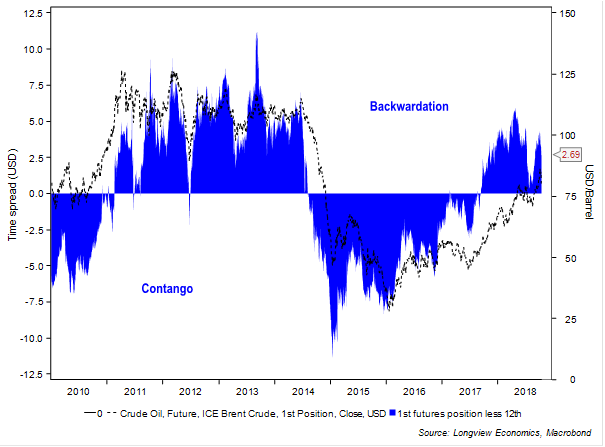

In oil, prices have opened higher this week reflecting rising geopolitical tension, as a result of the missing Saudi journalist. That price rise has occurred despite elevated net LONG positioning and a continued unwind of that high net LONG WTI positioning (fig 21); similarly, backwardation in the curve has also recently subsided (FIG C). Our work suggests that while the medium term bull case for oil remains intact, in the near term (barring a significant supply shock by Saudi Arabia in response to US sanctions or similar measures) the oil price should trade sideways/weaken (for detail see Commodity Fundamentals Report No. 86, 11th Oct 2018: “US bottlenecks easing, Iranian sanctions overblown”).

Despite the impasse in talks between the UK and EU, sterling has rallied back from overnight weakness. That likely reflects the elevated net SHORT positioning. While in the medium term we expect sterling to weaken reflecting the poor outlook for the UK economy, in the near term the current positioning could act as fuel for a relief rally (for more detail on the UK economy see Global Macro Report, 10th October 2018: “UK: The Economy Beyond Brexit”).

FIG C: Backwardation/contango in the Brent futures curve (1st less 12th position)

FIG D: VIX vs. net speculative LONG/SHORT positions

Points of note

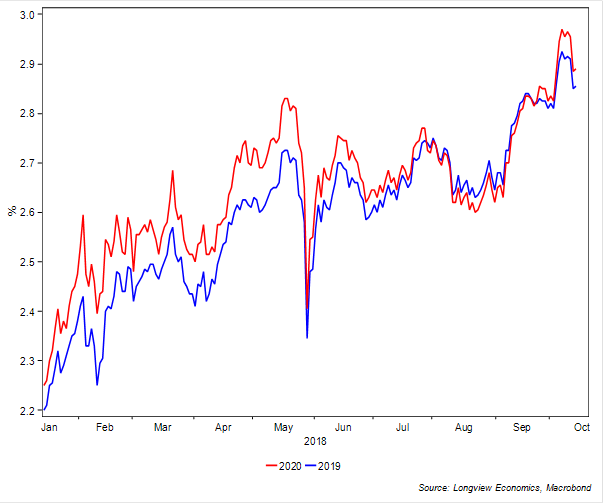

Bonds/rates: Treasury prices, having sold off for the prior month, rallied last week as risk aversion swept global markets. With that, net SHORT speculative positioning was reduced across all the maturities that we track (except the 5 year in which it increased to a record high, figs 1 – 4). Despite weakness in global risk assets, future US interest rate expectations only moved modestly (e.g. see 2019 & 2020 Fed funds futures, FIG C). Our work on the US economy suggests that the Fed could pause their current path of monetary tightening given signs of slowing growth (for detail see US extract from Q3 quarterly asset allocation, 14th Sep 2018: "The Fed: Gearing up for a Pause a.k.a. Mute Underlying Inflation"). As such we recommended moving LONG US 10 & 30 year bond futures last week (for detail see Macro Trade Recommendation No. 93, 11th Oct 2018: “Start BUILDing LONG Bond Positions”).

FIG E: Implied (using futures) December 2019 & 2020 average Fed funds rate

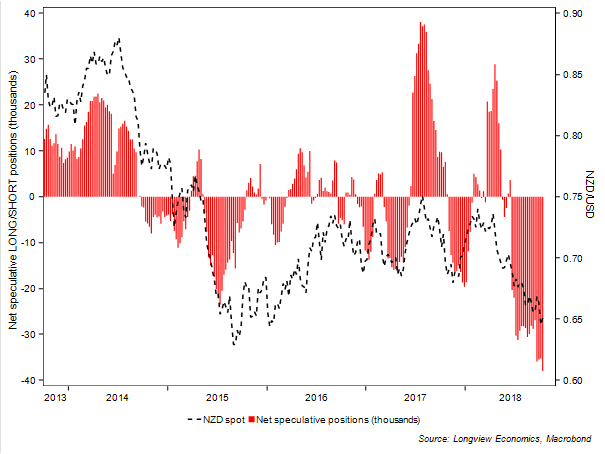

Currencies: Net SHORT positioning in the JPY was increasingly elevated going into last week’s bout of risk aversion (fig 12). As a safe haven asset the yen subsequently strengthened wrongfooting speculators. In contrast, net SHORT positioning in the CHF, another defensive currency, has significantly unwound in recent months (albeit it increased last week, fig 14). In the AUD and NZD, net SHORT positioning is the highest since 2015 and the highest on record respectively (figs 15 & FIG E). These currencies historically have been highly correlated.

Commodities: In copper, net LONG positioning reduced modestly last week as the copper price gave back some of its recent gains (fig 24). Copper has held up surprisingly well given the weakness in other China related assets, e.g. the Shanghai Composite which fell over 9% last week. Given slowing Chinese credit growth, we expect the copper price to weaken in the medium term and speculative LONG positioning to unwind further (for detail see Commodity Fundamentals Report No. 83, 12th July 2018: “Copper & Chinese credit growth: Going lower”).

FIG F: NZD-USD vs. net speculative LONG/SHORT positions

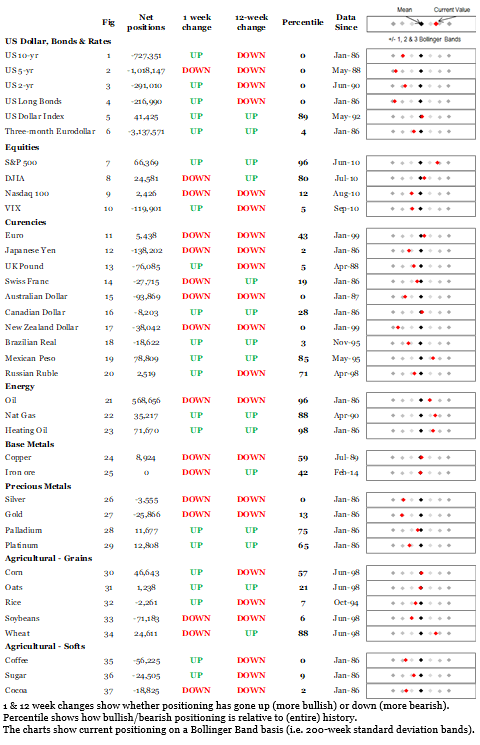

Summary table:

Please see HERE for charts of positioning in a wide variety of assets